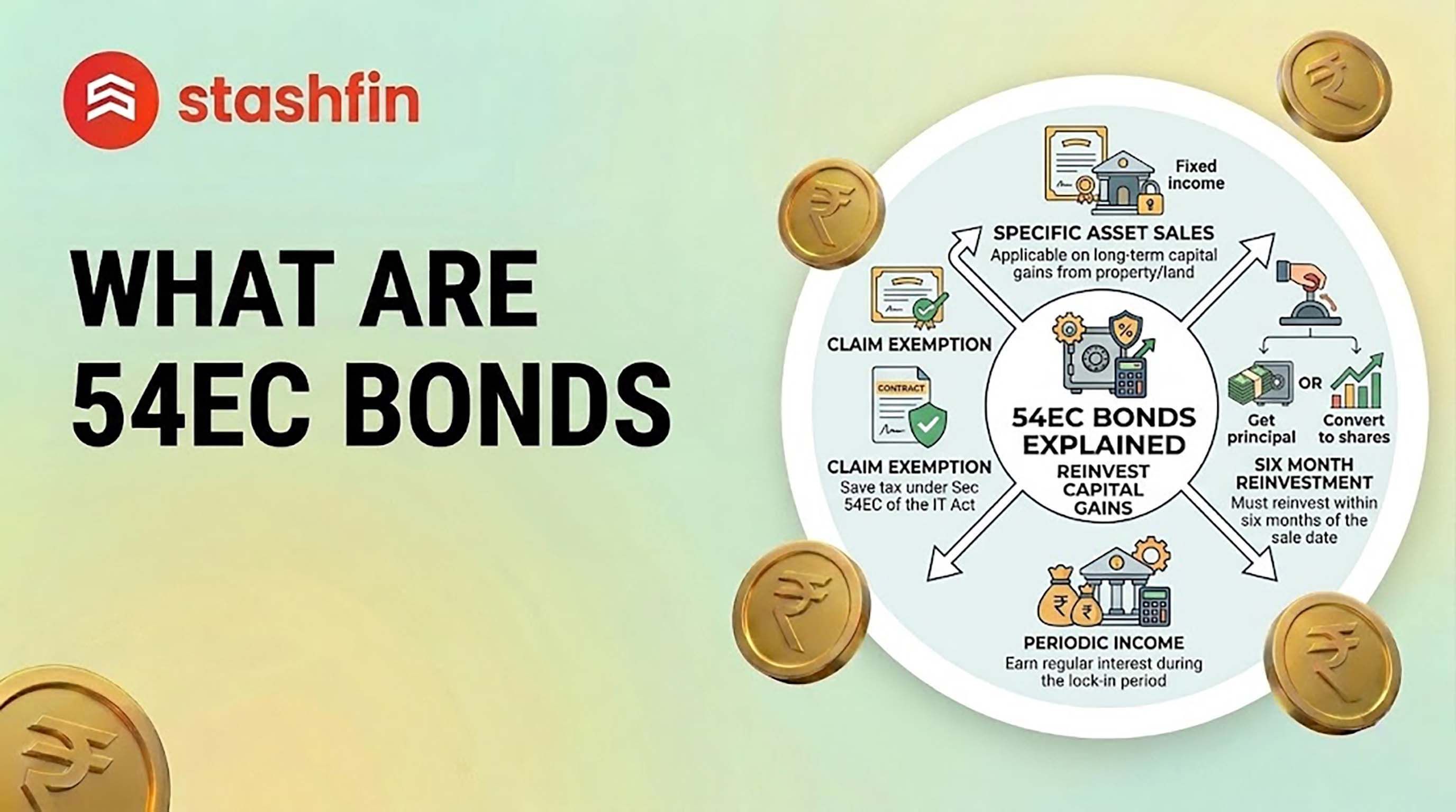

What Are 54EC Bonds?

54EC Bonds are specialised investment instruments notified under Section 54EC of the Income Tax Act, 1961. They are specifically designed for taxpayers who have earned capital gains from the sale of immovable property (land, building, or both) and wish to reinvest those gains to claim a tax exemption.

By investing the LTCG (Long-Term Capital Gain) amount into these bonds, you can legally avoid paying the 12.5% tax (the prevailing rate in 2026) on your gains. This makes them one of the most popular tax-saving havens for property sellers who do not wish to reinvest in another residential house.

This 2026 investor’s guide demystifies 54EC Bonds for property sellers in India. Learn about the ₹50 Lakh investment cap, the mandatory 5-year lock-in, and why AAA-rated bonds from PSU giants like REC, PFC, IRFC, and HUDCO are the safest way to save up to ₹6.25 Lakh in tax this financial year.

How Section 54EC Bonds Work: The 6-Month Rule

To qualify for the tax exemption, you must follow a strict timeline and set of rules. As of 2026, the process is highly streamlined but requires precision.

- The 6-Month Window: You must invest the capital gains into these bonds within 6 months from the date of the property transfer. Missing this deadline by even a day disqualifies you from the tax benefit.

- Asset Type: The exemption is only available on gains arising from the sale of land or buildings (residential or commercial). It does not apply to gains from stocks, gold, or mutual funds.

- The Holding Period: The property sold must have been held for at least 24 months to be classified as a long-term capital asset.

Key Features of 54EC Bonds in 2026

In the current 2026 fiscal environment, these bonds offer a "safety-first" approach for conservative investors.

| Feature | Details (2026 Context) |

|---|---|

| Current Interest Rate | 5.25% p.a. (Paid annually) |

| Lock-in Period | 5 Years (Non-negotiable) |

| Minimum Investment | ₹20,000 (2 Bonds) |

| Maximum Investment | ₹50 Lakh per financial year |

| Credit Rating | AAA/Stable (Highest Safety) |

| Mode of Holding | Demat or Physical Certificate |

The 2026 Tax Advantage: Calculating Your Savings

Under the current tax regime of 2026, the LTCG tax rate is 12.5% without indexation for properties sold after July 2024.

Example: Suppose you sold a plot of land and realized a profit of ₹40 Lakh.

- Without 54EC Bonds: You would owe the government ₹5 Lakh (12.5% of ₹40 Lakh).

- With 54EC Bonds: You invest the ₹40 Lakh in REC or PFC bonds. Your tax liability becomes Zero. You save ₹5 Lakh instantly and earn an additional ₹2.10 Lakh in interest over the next 5 years.

Eligible Issuers: Where Can You Invest?

Only specific government-backed Public Sector Undertakings (PSUs) are authorized by the RBI to issue these bonds. In 2026, the active issuers are:

- REC (Rural Electrification Corporation Ltd)

- PFC (Power Finance Corporation Ltd)

- IRFC (Indian Railway Finance Corporation Ltd)

- HUDCO (Housing and Urban Development Corporation Ltd)

- IREDA (Indian Renewable Energy Development Agency)

Note: NHAI (National Highways Authority of India), once a major player, has discontinued new 54EC bond issues as of 2026.

Critical Constraints: The Fine Print

While the tax savings are attractive, 54EC bonds are not "liquid" assets. Investors must be aware of the following:

- Non-Transferable: You cannot sell these bonds in the secondary market (stock exchange) during the 5-year lock-in.

- No Loan Facility: You cannot pledge these bonds as collateral for a bank loan or any credit line.

- Taxable Interest: While the principal investment is tax-exempt, the 5.25% annual interest you receive is added to your income and taxed at your applicable slab rate. However, no TDS (Tax Deducted at Source) is applied by the issuers.

How to Invest in 54EC Bonds Today

In 2026, the investment process has moved largely online through the "Direct" portals of the issuers.

- Choose Your Issuer: Most investors pick based on the interest payment date (e.g., REC pays in June, IRFC in October).

- Application: Visit the issuer’s website (e.g., REC’s "Sugam" portal) or use a regulated bond platform.

- KYC: Complete your digital KYC using your PAN, Aadhaar, and a cancelled cheque.

- Payment: Transfer the funds via NEFT or RTGS. Ensure the payment comes from the bank account of the primary bondholder.

- Allotment: The bonds are typically credited to your Demat account within 4-6 weeks.

Conclusion

54EC Bonds are the "safety anchors" of property tax planning. They allow you to defer your tax liability, protect your principal with AAA-rated PSU security, and earn a steady 5.25% return. In 2026, as the indexation benefit has been removed for many, these bonds represent one of the last remaining "clean" ways to save up to ₹6.25 Lakh in tax on a ₹50 Lakh gain.

Would you like me to help you compare the current interest payout dates of REC and IRFC to see which fits your cash flow better?