Home Loan Tax Benefits in India: Deductions Under Section 24, 80C & 80EE (2026 Guide)

Audience Analysis: The Mid-Career Homeowner

The primary persona for this guide is the "Mid-Career Homeowner." You are likely a salaried professional (30–45 years old) who has either recently purchased a home or is in the peak years of loan repayment. You understand the basics of income tax but are looking for a deep dive into how to maximize every available rupee in tax savings as the 2026-27 Assessment Year approaches. You value clear, expert advice that bridges the gap between complex tax laws and your monthly bank balance.

Quick Summary: Home Loan Tax Savings at a Glance

Before we dive into the deep dive, here is the "Cheatsheet" to understand how much you can shield from the taxman this year.

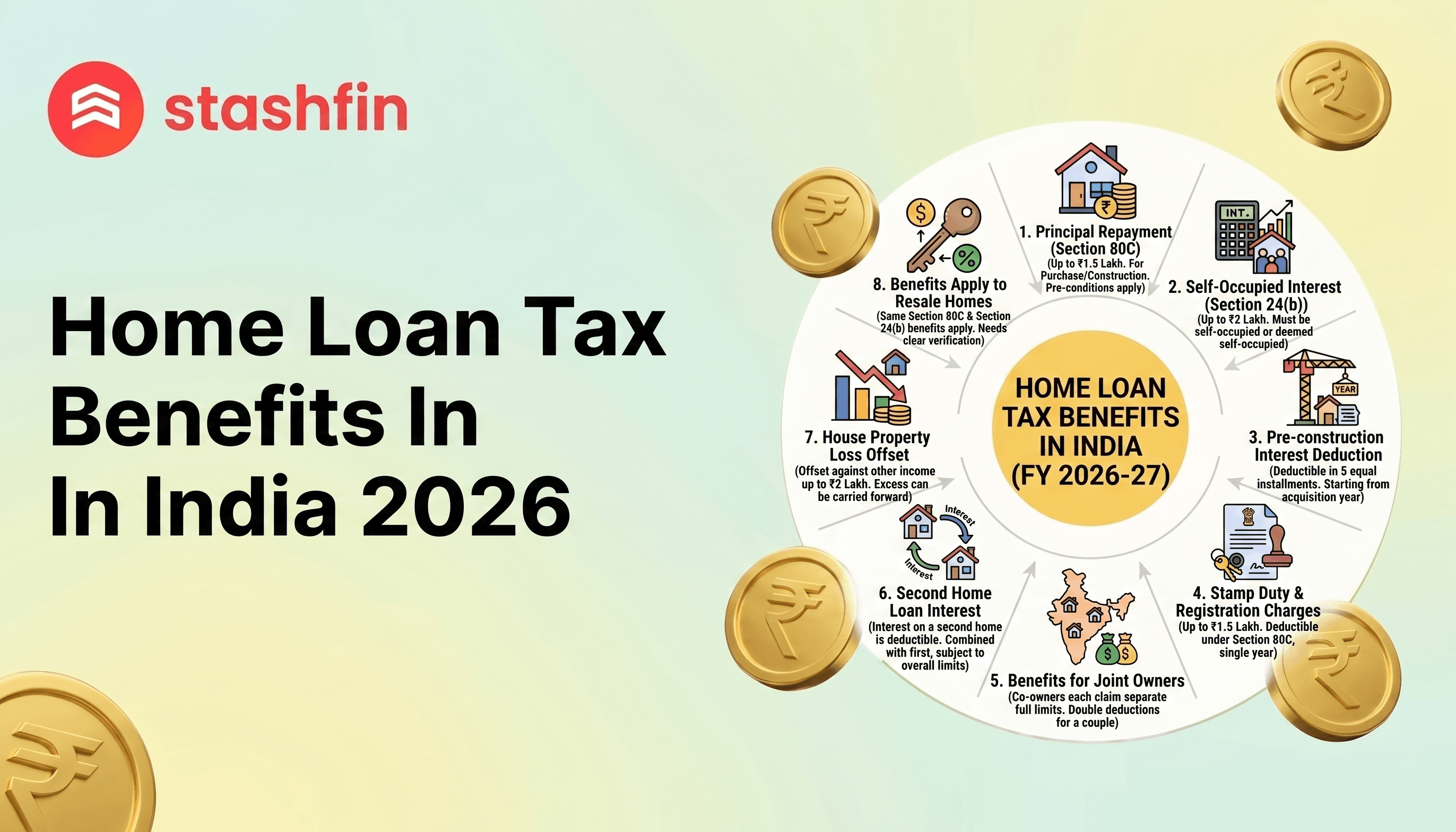

- Principal Repayment: Claim up to ₹1.5 Lakh under Section 80C. This includes your stamp duty and registration charges (in the year of purchase).

- Interest Component: Claim up to ₹2 Lakh for a self-occupied property under Section 24(b).

- Joint Ownership: If you co-own and co-borrow with a spouse, you can double these benefits (up to ₹7 Lakh combined deduction for the household).

- First-Time Buyers: Additional deductions of up to ₹50,000 (under Section 80EE) or ₹1.5 Lakh (under Section 80EEA) may apply based on specific windows.

- Regime Choice: Most benefits are only available under the Old Tax Regime. Under the New Tax Regime (the 2026 default), interest deductions are limited to let-out properties.

1. Section 24(b): The "Interest" Powerhouse

Section 24(b) allows you to deduct the interest portion of your Home Loan EMI from your "Income from House Property."

The ₹2 Lakh Limit: Self-Occupied Property

If you live in the house for which you took the loan, the maximum interest you can deduct is ₹2,00,000 per financial year.

The "No Limit" Rule: Rented Property

If you have let out your property, there is no upper limit on the interest deduction. However, if this results in a "loss," you can only set off up to ₹2 Lakh of that loss against other income heads (like salary) in a single year; the rest can be carried forward for 8 years.

The 5-Year Construction Clause

Construction must be completed within 5 years from the end of the financial year the loan was taken. If it takes longer, the deduction drops to ₹30,000.

Expert Tip: If a budget shortfall is delaying completion, a Stashfin Personal Loan (up to ₹5 Lakh) can provide the liquidity needed to finish on time, ensuring you don't lose out on lakhs in tax benefits.

2. Section 80C: Saving on the Principal

Section 80C is where you claim the Principal Repayment portion of your EMI.

- The ₹1.5 Lakh Umbrella: This limit is shared with EPF, PPF, Life Insurance, and ELSS.

- Stamp Duty and Registration: These charges are deductible under 80C, but only in the year they are paid and within the overall ₹1.5 Lakh limit.

3. Sections 80EE & 80EEA: The First-Time Buyer's Bonus

These offer benefits over and above Section 24(b) for eligible borrowers.

| Section | Deduction Limit | Loan Sanction Window | Property Value Limit |

|---|---|---|---|

| 80EE | Up to ₹50,000 | April 2016 – March 2017 | Value ≤ ₹50L; Loan ≤ ₹35L |

| 80EEA | Up to ₹1,50,000 | April 2019 – March 2022 | Stamp Value ≤ ₹45L |

4. Joint Home Loans: The Ultimate Tax Hack

By buying a house jointly with your spouse, each co-owner (who is also a co-borrower) can claim deductions separately.

Solo vs. Joint Tax Benefits (FY 2026-27)

| Benefit Type | Solo Applicant (Max) | Joint Applicants (Max Total) |

|---|---|---|

| Section 24(b) - Interest | ₹2,00,000 | ₹4,00,000 (₹2L each) |

| Section 80C - Principal | ₹1,50,000 | ₹3,00,000 (₹1.5L each) |

| Total Deduction | ₹3,50,000 | ₹7,00,000 |

| Approx. Tax Saved (30% slab) | ~₹1,08,000 | ~₹2,16,000 |

5. Pre-Construction Interest: Claiming Before You Move In

Interest paid before getting possession is "Pre-construction interest."

- The 5-Installment Rule: Once construction is complete, you can claim the total pre-construction interest in 5 equal annual installments.

- The Cap: The total claim (current interest + 1/5th pre-construction) is still capped at ₹2 Lakh for self-occupied homes.

6. When Tax Benefits Get Reversed

- Selling within 5 Years: If you sell within 5 years of possession, all Section 80C deductions claimed previously will be added back to your income and taxed in the year of sale.

- Section 24: Interest deductions are not reversed even if the house is sold early.

7. Navigating the 2026 Tax Regimes

As of 2026, the New Tax Regime is the default.

- Old Regime: Includes 80C, 24(b), and 80EEA. Usually better if total deductions exceed ₹4 Lakh.

- New Regime: No 80C or 24(b) for self-occupied houses. Only interest on let-out properties is allowed (capped at rental income).

8. Strategic Financial Planning with Stashfin

- Down Payment Gaps: Use a Stashfin Credit Line for instant access to funds for registration fees.

- Invest the Savings: Reinvest your tax refund into Akara Capital Bonds for higher returns to pay off your loan faster.

- Credit Health: Maintain top-tier credit scores for both joint applicants using Stashfin’s Credit Health reports to secure the best interest rates.

Conclusion

Mastering home loan tax benefits in 2026 requires a 360-degree view of the law. By strategically timing your purchase and opting for joint ownership, you can turn debt into a highly efficient tax-saving instrument.

Frequently Asked Questions (FAQs)

1. Can I claim both HRA and Home Loan tax benefits?

Yes, if you live in a rented house while your owned property is in another city or under construction. If in the same city, you need a valid reason like workplace distance.

2. Is the ₹2 Lakh interest limit per house or per person?

It is per person. Joint owners each get a ₹2 Lakh limit.

3. Do I get tax benefits on a home renovation loan?

Under Section 24(b), you can claim interest up to ₹30,000 per year. Principal repayment for renovation is not eligible for 80C.

4. What documents do I need?

You need the Interest Certificate from your lender, the Completion Certificate, and proof of Stamp Duty payment.

5. Can I claim tax benefits if I miss an EMI?

Section 24(b) (interest) is based on accrual (payable), so you can claim it. Section 80C (principal) is strictly on a payment basis.